If you have been thinking about buying a home, you no doubt have lots of questions, especially about interest rates and how they will affect the process positively and/or negatively. However, if you are like most people, you don’t buy a house very often; therefore, it’s hard to keep up with the ever-changing trends in the market, as well as the mortgage industry.

The fha refinance program has been more popular than ever the last few years as credit has become harder to get. FHA loans are one of the best options available for borrowers that would like to refinance their mortgage to get a better deal or to pay off debt. FHA loans are known as an easy loan to qualify for due to the flexible credit guidelines and the low equity requirements.

But that’s OK because we are going to discuss interest rates and how they affect the housing market, the impact they have on the industry as a whole, what happens when the interest rates rise, and more.

How Interest Rates Impact the Housing Market

How Interest Rates Impact the Housing Market

Interest rates are determined by the Federal Reserve and the interest percentage is what determines the rate money can be borrowed which includes buying a house. Therefore, when the interest rates are low, the trend moves towards more people buying homes. And when the rates increase, buying becomes more expensive and will usually slow down the buying trend. However, how slow is a direct reflection on how much those rates have risen or are predicted to rise.

Other factors include when interest rates are low, people with high-interest rates on their existing mortgages will attempt to refinance their mortgages which is great for the industry. Additionally, when interest rates are low, generally, more homes are built because the demand for them rises. And because new home builders are able to borrow money at a cheaper rate.

So pretty much, the entire housing market, in a way, revolves around what the interest rates are doing at the time.

Do Rising Interest Rates Hurt the Real Estate Industry

Well, yes and no.

Rising interest rates, as we mentioned above, make buying a home more expensive; therefore, the sale of homes generally declines. So in this case, yes, it can hurt the real estate industry somewhat. However, it really depends on how much and how often the rates go up, and, if the rates continue to go up, which is another story we will talk about in a moment.

Now, with that being said, there is another side to rising interest rates that tend to counteract those effects. Which means, when the interest rates rise, home appreciation does not stop. It continues to rise. So the house you paid a bit more for is continually appreciating in value because rising interest rates don’t affect that aspect of the housing market.

Other factors that come with rising interest rates, is that they generally happen because the economy is strong, which in turn, results in lower unemployment rates and higher wages that result in more people being able to buy a house. Not to mention the millennials who have, on average, $88,000 in an annual household income and are now the largest segment entering the home buying market. More about that in a moment.

This is all really good news regardless of the recent interest rate hikes, which are still historically low. Did you know the interest rate in 1981 was almost 19 percent? Ouch! Be glad you were not trying to buy a home back then. And if you were, be glad that times have changed for the better. Much better!

Do Rising Interest Rates Mean Lower Home Prices?

It seems, from a common sense standpoint, if interest rates go up, that the price of homes would go down. And this is true to some extent. However, there’s more to it than that. Rising interest rates actually have the opposite effect. As we mentioned above, interest rates go up when the economy is strong, resulting in lower unemployment rates and higher wages, as well as the steady increase in home appreciation rates. This means people can afford to buy bigger, better homes and are more willing to accept larger mortgages to pay for them.

There are other factors that also affect home prices, which include the available inventory and how much it costs home builders in construction prices to actually build their homes.

So…do rising interest rates mean lower home prices?

No…not always!

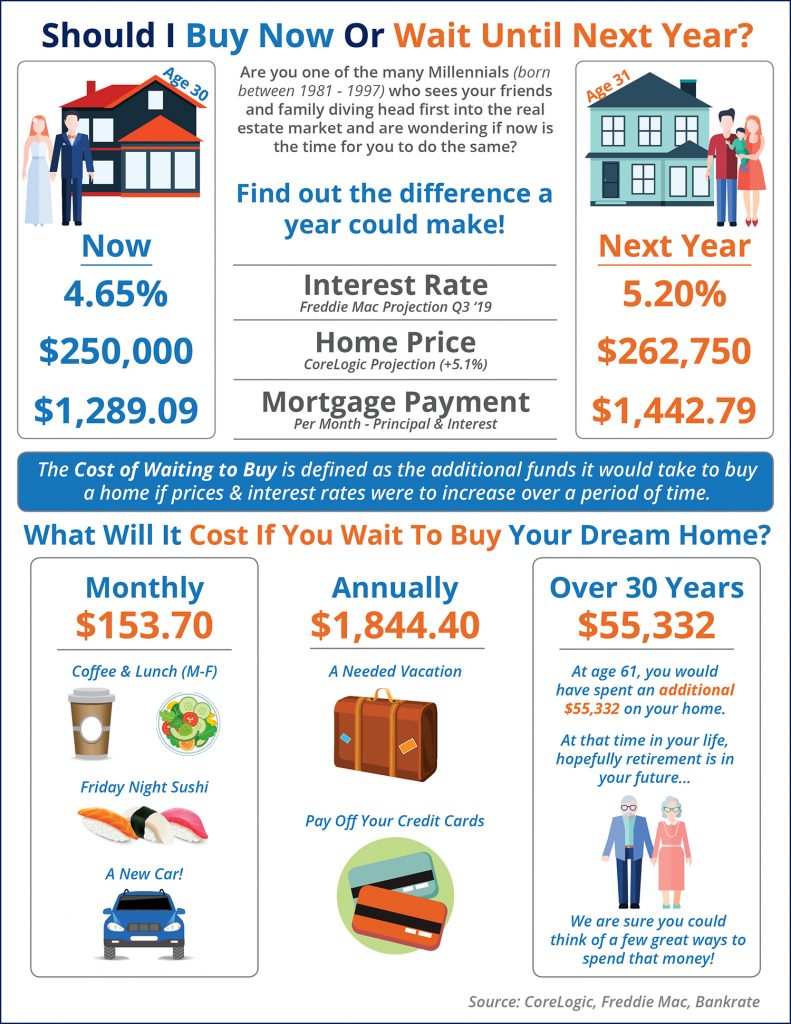

How Much Rising Interest Rates Cost Homebuyers

As you know, when the interest rates rise, it will cost homebuyers more to buy a home. This issue is aside from the continual rise in the home appreciation values we talked about a minute ago. These are separate issues.

Generally, when interest rates go up, homebuyers lose their purchasing power because homes cost more which means the buyer gets less home for their money. Because, if a buyer only has so much budgeted for housing per month, they now have to settle for a lesser home to compensate for the higher interest rates and higher-priced mortgage. That means the better home might now be out of the buyer’s price range.

For example, according to Marketwatch and Redfin, “A buyer with a $2,500 monthly housing budget lost nearly $30,000 in purchasing power last year.” This is because if they had a $2,500 a month budget and a 20% down payment, that buyer could, at the beginning of last year afford to buy a house for as much as $473,500 when the mortgage interest rates were lower. But now that the interest rates have risen, that same buyer can only afford to buy a house that is priced up to $444,000, which is a loss of almost $30,000.

This is what is meant by a loss of purchasing power when the interest rates go up. That, coupled with the number of affordable homes on the market dwindling by approximately 25 percent in cities like San Diego, means that buyers should not wait to buy a new home. If they do, they will ultimately have to pay more (unless the interest rates drop), provide a larger down payment, or settle for a lesser home, if they can find one at all.

THE EXCEPTION:

The one exception to this is buying a home in a hot market. For example, according to Realtor.com, the housing market in Lakeland, Florida is poised to remain hot in 2019. This is a direct result of the strong economy in Lakeland and the number of affordable homes on the market. In addition, Lakeland has been named the #1 city for buying a house according to Business Insider. All because of the growing number of jobs, vigorous construction, and the large number of young homebuyers moving in.

Wait…what?

Why does the age of homebuyers in any given market even matter?

Let’s look at that.

Millennials Are Now Entering the Home Buying Market

Different segments of the market affect home buying differently. The segment of the population entering the peak or at the peak of their earning years account for the most sales in the market. For example, Baby Boomers are retiring and downsizing. This means there are more homes on the market for millennials to scoop up. And, as we mentioned above, millennials (those born between 1981-1996) are the segment of the population entering their peak earning years and currently make an average household income of $88,000 per year. This is also the age when most people need to buy a home due to getting married and starting a family or having to accommodate a growing family.

Different segments of the market affect home buying differently. The segment of the population entering the peak or at the peak of their earning years account for the most sales in the market. For example, Baby Boomers are retiring and downsizing. This means there are more homes on the market for millennials to scoop up. And, as we mentioned above, millennials (those born between 1981-1996) are the segment of the population entering their peak earning years and currently make an average household income of $88,000 per year. This is also the age when most people need to buy a home due to getting married and starting a family or having to accommodate a growing family.

However, the millennials are still behind in their numbers when it comes to homeownership compared to other generations. This is due to a mix of socioeconomic issues such as getting married later than other generations, they have more student loan debt, and they increasingly live in more expensive cities. And that doesn’t take into account the home buying myths younger buyers tend to believe as truth.

For example, some believe they can’t afford to save for a down payment, and they can with the right bank. Additionally, many millennials don’t realize that a 20% down payment is no longer required and that they can now qualify to purchase a home with much less money down. In fact, with an FHA loan, which is common, especially for first-time homebuyers, a mortgage can be obtained with as little as 3.5% down. In addition, there are plenty of first-time homebuyer down payment assistance programs out there for those who qualify.

So what it all really boils down to is…if you are interested in buying a home, don’t wait. Now is the time to buy. Which means you should contact a real estate agent immediately, even if you don’t think you make enough money, don’t have enough money to put down, or think that it’s impossible. A real estate agent will know all the tricks of the trade and might be able to get you into a new home much sooner than you thought possible. Remember, if you wait, it will probably cost you more money to buy a home. So consider buying now versus waiting.

OK, that all sounds great, but what if the interest rates continue to go up?

What Happens if the Interest Rates Continue to Rise?

Even though the Federal Reserve has stated they are temporarily pausing interest rate hikes, we all know they will continue to rise at some point, probably sooner rather than later. However, with that being said, the housing market in its current condition is able to handle rising interest rates due to the strong economy, rising incomes, housing price trends, and the fact that the health of the overall housing market is in great financial shape. In addition, because of the current health of existing home sales and less risky lending practices such as the ones that were used in the mid-2000s like zero down mortgages, interest-only mortgages, and mortgage flipping, a crash such as that one is unlikely.

The general rule of thumb is if the economy is strong and doing well, the housing market is usually strong as well. Not to mention the low available home inventory which is another factor that strengthens the housing market. Therefore, with all these economic indicators in place, even if the interest rates rise, it shouldn’t negatively affect the housing market too much.

Tips for Buying a Home Now

By now, you have probably realized it’s better to go ahead and buy your new or next home now rather than waiting. However, there are a few steps you should take immediately that will help make your home buying journey a little easier.

- Contact a local real estate agent.

- Review your income and expenses.

- Determine how much you can afford to spend on a home, including a comfortable monthly payment and how much you have to put down.

- Don’t forget to budget for transitional costs such as month-to-month fees (if you rent), interim housing in case you sell your current home before your new home is ready and/or available, moving expenses, lawn equipment or additional furniture for your new home, etc.

- Check your credit reports and make any corrections necessary.

- Compare mortgage lenders to get the best possible rate.

Remember, if you have a question, don’t hesitate to ask your real estate agent. No question is too silly or too small. Additionally, if you find the home of your dreams and for whatever reason, it doesn’t work out…don’t dwell on it. There will always be another home out there. Quite possibly a better one. So don’t get discouraged.

What’s Next?

If you don’t want to wait to buy your new home, please Contact Us today. We can provide you with a list of homes that meet your wants, needs, and budget. In addition, we would be happy to give you a free home valuation for your current home and a market comparison to help get you started.

What are you waiting for? Call now. We would love to show you just how fun and exciting buying a new home can be.

Additional Resources About Mortgage and Home Buying!

- Should I go with a mortgage broker or a bank? – Conor MacEvilly

- Tips on How to Get The Best Mortgage Rate – Bill Gassett

- What Every Loan Officer Wished Their Home Buyers Knew – Kevin Vitali

- Saving For A Down Payment – Luke Skar

____________________________________________________________________________________________________

About the author: The above real estate article “How Mortgage Rates Affect Home Buying Now and Going Forward” was written by Petra Norris of Lakeland Real Estate Group, Inc. With over 20 years of combined experience of selling or buying, we would love to share our knowledge and expertise. Petra can be reached via email at petra@petranorris.com or by phone at 863-712-4207

We service the following Central Florida areas: Lakeland, Auburndale, Mulberry, Winter Haven, Bartow, Plant City, Seffner, Valrico, Polk City, Lake Alfred, Lake Wales, Haines City, and Davenport FL.

Excellent information about mortgage rates. The good news for the moment is that buyers may have a bit more time before rates continue to climb higher.

Thank you Gabe! Yes, just a bit more time. However, I would not wait too long as home prices do increase steadily.